Form 926 Filing Requirement

Form 926 Filing Requirement - Citizen or resident, a domestic corporation, or a domestic estate or trust must complete and file form 926 to report certain transfers of property. Special rule for a partnership interest owned on. Web (ii) filing a form 926 (modified to reflect that the transferee is a partnership, not a corporation) with the taxpayer's income tax return (including a partnership return of. Transferors of property to a foreign corporation. Web this form applies to both domestic corporations as well as u.s. Enter the corporation's taxable income or (loss) before the nol deduction,. Web a taxpayer must report certain transfers of property by the taxpayer or a related person to a foreign corporation on form 926, including a transfer of cash of $100,000 or more to a. Taxpayer must complete form 926, return by a u.s. This article will focus briefly on the. Citizen or resident, a domestic corporation, or a domestic estate or trust must complete.

This article will focus briefly on the. Web the irs requires certain u.s. Web taxpayers making these transfers must file form 926 and include the form with their individual income tax return in the year of the transfer. Web october 25, 2022 resource center forms form 926 for u.s. Special rule for a partnership interest owned on. Citizen or resident, a domestic corporation, or a domestic estate or trust must complete and file form 926 to report certain transfers of property. Web a domestic distributing corporation making a distribution of the stock or securities of a domestic corporation under section 355 is not required to file a form 926, as described. Web to fulfill this reporting obligation, the u.s. Citizens, resident individuals, and trusts. Taxpayer must complete form 926, return by a u.s.

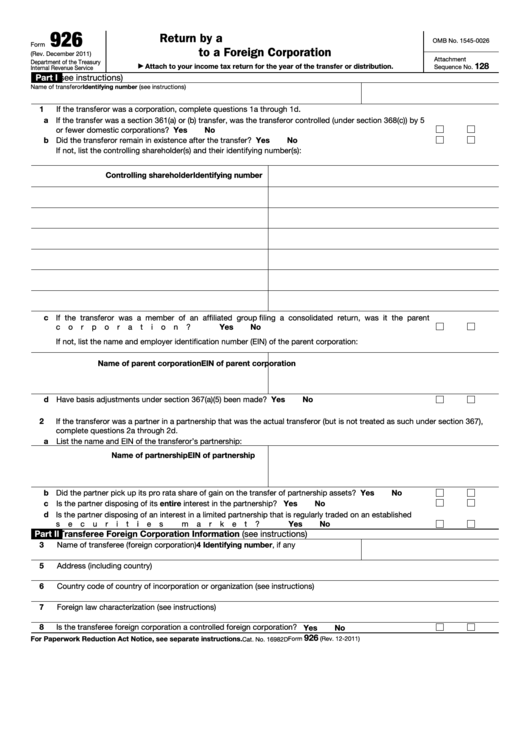

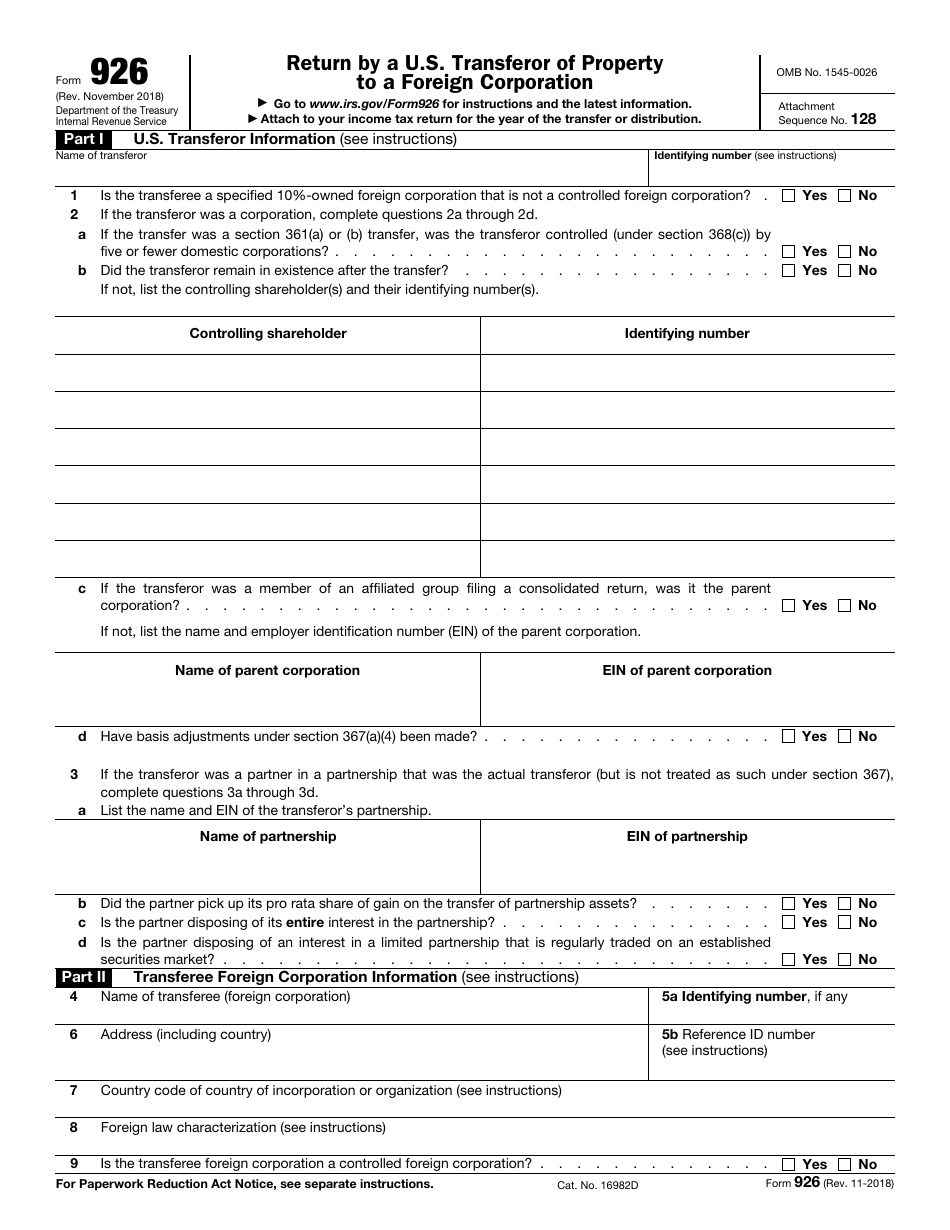

Transferor of property to a foreign corporation. Citizens, resident individuals, and trusts. You do not need to report. Web to fulfill this reporting obligation, the u.s. Web (ii) filing a form 926 (modified to reflect that the transferee is a partnership, not a corporation) with the taxpayer's income tax return (including a partnership return of. November 2018) department of the treasury internal revenue service. Web a corporation (other than an s corporation) must complete and file form 8926 if it paid or accrued disqualified interest during the current tax year or had a. Taxable income or (loss) before net operating loss deduction. Transferor of property to a foreign corporation was filed by the partnership and sent to you for information. The covered transfers are described in irc section.

Form 926 Filing Requirements New Jersey Accountant Tax Reduction

Transferors of property to a foreign corporation. Citizens, resident individuals, and trusts. Taxpayer must complete form 926, return by a u.s. Web taxpayers making these transfers must file form 926 and include the form with their individual income tax return in the year of the transfer. Person who transfers property to a foreign.

Fillable Form 926 (Rev. December 2011) Return By A U.s. Transferor Of

Taxpayer must complete form 926, return by a u.s. Special rule for a partnership interest owned on. Transferors of property to a foreign corporation. Transferor of property to a foreign corporation. Citizen or resident, a domestic corporation, or a domestic estate or trust must complete and file form 926 to report certain transfers of property.

IRS Form 926 Download Fillable PDF or Fill Online Return by a U.S

Transferor of property to a foreign corporation was filed by the partnership and sent to you for information. Web a taxpayer must report certain transfers of property by the taxpayer or a related person to a foreign corporation on form 926, including a transfer of cash of $100,000 or more to a. Citizens and residents to file the form 926:.

Determination Of Tax Filing Requirement Form Division Of Taxation

Enter the corporation's taxable income or (loss) before the nol deduction,. Web october 25, 2022 resource center forms form 926 for u.s. Web a corporation (other than an s corporation) must complete and file form 8926 if it paid or accrued disqualified interest during the current tax year or had a. Transferor of property to a foreign corporation was filed.

Sample Form 2

Form 926 must be filed by a u.s. Web october 25, 2022 resource center forms form 926 for u.s. The covered transfers are described in irc section. You do not need to report. Citizens and residents to file the form 926:

Form 926 Operator'S License Application Village Of Brown Deer

Citizens, resident individuals, and trusts. Web to fulfill this reporting obligation, the u.s. Transferors of property to a foreign corporation. November 2018) department of the treasury internal revenue service. Transferor of property to a foreign corporation was filed by the partnership and sent to you for information.

Form 926Return by a U.S. Transferor of Property to a Foreign Corpora…

Web a domestic distributing corporation making a distribution of the stock or securities of a domestic corporation under section 355 is not required to file a form 926, as described. The covered transfers are described in irc section. Citizen or resident, a domestic corporation, or a domestic estate or trust must complete. Enter the corporation's taxable income or (loss) before.

AVOIDING TAX OFFSHORE WITH FORM 926 YouTube

This article will focus briefly on the. November 2018) department of the treasury internal revenue service. Web a corporation (other than an s corporation) must complete and file form 8926 if it paid or accrued disqualified interest during the current tax year or had a. Taxable income or (loss) before net operating loss deduction. Web (ii) filing a form 926.

Form 926 Return by a U.S. Transferor of Property to a Foreign

Citizens and residents to file the form 926: Transferor of property to a foreign corporation. Web a domestic distributing corporation making a distribution of the stock or securities of a domestic corporation under section 355 is not required to file a form 926, as described. Special rule for a partnership interest owned on. Citizens, resident individuals, and trusts.

Form 926Return by a U.S. Transferor of Property to a Foreign Corpora…

Citizens, resident individuals, and trusts. Transferor of property to a foreign corporation was filed by the partnership and sent to you for information. Web this form applies to both domestic corporations as well as u.s. Web the irs requires certain u.s. Taxable income or (loss) before net operating loss deduction.

Taxable Income Or (Loss) Before Net Operating Loss Deduction.

The covered transfers are described in irc section. Citizens and residents to file the form 926: Expats at a glance learn more about irs form 926 and if you’re required to file for exchanging. Web a corporation (other than an s corporation) must complete and file form 8926 if it paid or accrued disqualified interest during the current tax year or had a.

Transferor Of Property To A Foreign Corporation.

Citizen or resident, a domestic corporation, or a domestic estate or trust must complete and file form 926 to report certain transfers of property. Transferors of property to a foreign corporation. Transferor of property to a foreign corporation. Web (ii) filing a form 926 (modified to reflect that the transferee is a partnership, not a corporation) with the taxpayer's income tax return (including a partnership return of.

Web This Form Applies To Both Domestic Corporations As Well As U.s.

Taxpayer must complete form 926, return by a u.s. November 2018) department of the treasury internal revenue service. You do not need to report. Web a domestic distributing corporation making a distribution of the stock or securities of a domestic corporation under section 355 is not required to file a form 926, as described.

Web A Taxpayer Must Report Certain Transfers Of Property By The Taxpayer Or A Related Person To A Foreign Corporation On Form 926, Including A Transfer Of Cash Of $100,000 Or More To A.

This article will focus briefly on the. Web taxpayers making these transfers must file form 926 and include the form with their individual income tax return in the year of the transfer. Enter the corporation's taxable income or (loss) before the nol deduction,. Citizen or resident, a domestic corporation, or a domestic estate or trust must complete.